Under the current UK retail product disclosure regime, manufacturers of Packaged Retail and Insurance-based Investment Products ("PRIIPs") (such as shares in VCTs and Investment Trusts) are required to produce a standardised Key Information Document ("KID"), which must be provided to investors prior to any transaction. These documents have strict requirements which they must adhere to, dictating what must be included, and in what format. Similar strict disclosure rules apply under the Undertakings for Collective Investment in Transferable Securities ("UCITS") regulations.

The new Consumer Composite Investments ("CCI") framework will replace both the PRIIPs and UCITS disclosure regimes with a single, UK-specific framework designed to better meet the needs of UK retail investors.

The framework is established by the Consumer Composite Investments (Designated Activities) Regulations 2024 (the "CCI Regulations") and accompanying FCA Handbook rules. It reflects the FCA’s view that existing disclosure documents are often overly complex, contain excessive legal jargon, and are insufficiently engaging for consumers. A recognition by the regulator by the existing regime is flawed. The new regime has therefore adopted a more flexible and proportionate approach, with a stronger emphasis on consumer understanding. Regulation has not, however, completed disappeared as, while those caught by the new regime will benefit from increased flexibility in presenting disclosures, certain core information to be disclosed will remain standardised to facilitate comparison across the various financial products.

The CCI Regulations came into effect on 6 April 2026 allowing optional adoption of the new product summary format, however continued compliance with the existing disclosure rules is permitted until 8 June 2027 when the regime comes fully into force. This post has been designed to provide an overview of the new requirements in preparation for compulsory compliance next year.

What is a Consumer Composite Investment ("CCI")?

A CCI is broadly defined by the FCA as

"an investment where returns are dependent on the performance of, or changes in, the value of underlying or reference assets".

Although there is no complete list of all products that will be captured as CCIs, the FCA has confirmed the following are within this scope:

- Open-ended funds

- Closed-ended funds (such as VCTs and Investment Trusts)

- Recognised funds

- Structured products and deposits

- Contracts for Difference (CFDs)

- Insurance-Based Investment Products (IBIPs)

- Other complex products (e.g. derivatives)

This scope is somewhat further defined by the specific exclusions the CCI Regulations have provided, including vanilla corporate bonds, pension products and pure protection insurance contracts. However, it must be emphasised that the non-exhaustive nature of these examples means each product must be assessed on a case-by-case basis to determine if it will indeed be classified as CCI under the new regime.

Disclosure Requirements

The CCI regime replaces PRIIPs KIDs, UCITS KIIDs, and NURS-KIIs with a new “product summary”, for all products targeted to retail investors within the UK. This will primarily affect firms that manufacture or distribute such products within the UK. While both will have responsibilities under the new regime, it is expected that the Alternative Investment Fund Manager ("AIFM") will prepare the product summary, with responsibility for doing so assigned to them by a written agreement. In the case of funds, including VCTs and Investment Trusts, this will almost always by the AIFM rather than the fund itself.

Manufacturers, or the AIFM, will note much greater flexibility in the design of the summary than was required under the previous regulations. Under the new CCI Regulations, the requirements for the summary simply state:

“…a short and concise document in English, titled ‘product summary’, setting out appropriate information about the essential characteristics of the consumer composite investment, conveying as a minimum the core information disclosures.”

As this suggests, there is no strict format for the document and instead manufacturers may design the summary in the way they feel best informs investors and supports the commercial position of their company. The summary must focus on key information necessary for informed decision making, using clear, simple consumer friendly language to portray this. Manufacturers must also have regard to the intended audience for the document, UK retail investors, and ensure it supports their understanding in line with the FCA's consumer duty avoiding unnecessary complexity or duplication.

The new regime does not allow complete free reign, however. The rules state product summaries must still include:

- A description of the investment objectives and policy;

- Risk and return information, including a risk rating on a 1–10 scale;

- Past performance data;

- Costs and charges;

- Product identification details;

- Details of the document’s preparer and issue date; and

- Information regarding the Financial Ombudsman Service and Financial Services Compensation Scheme ("FSCS"), where applicable.

Risk and Return Information

The CCI Regulations provide a new methodology to be used to calculate a product's risk and return score. Manufactures, or those preparing product summaries, are expected to use this new methodology to self-assess and determine the correct risk and return score.

Certain products, however, have been assigned pre-set minimum risk and return scores, making this requirement much less onerous. The FCA has allocated a risk and return score of 9 out of 10 for VCTs and EISs which must be stated within the product summary as a minimum.

Past Performance Data

While the FCA does not dictate how most information is provided, the CCI Regulations do stipulate that past performance data must be presented in a line graph format which will be supported by supplementary text of explanatory information. This data must cover a period for up to 10 years, and be calculated on a consistent basis throughout this time frame. If the product has not existed for this full period, the information should instead cover the entire life of the product. The data must be as up to date as possible, with the covered period ending no more than 60 days before preparation of the summary.

For funds including investment companies, there is a further requirement that performance data should be provided on the basis that income distributions are reinvested.

Finally, if the company is listed, it must also show the NAV total return on the graph and how this has changed over the period.

Costs

The following costs information much be disclosed:

- The ongoing costs figure;

- Any one-off entry costs;

- Any one-off exit costs;

- Transaction costs; and

- Performance fees and carried interest.

While all must be included within the summary, the regulations stress the importance of the ongoing costs figure, and state that this must be included as the headline figure; however, all other figures can be presented as seen fit, with no requirement for all costs to be in one location within the document.

For a listed fund such as a VCT which regularly conducts secondary share issues under an FCA approved Prospectus, much of the required information can be drawn from that document.

In line with the principals behind the change, the way this is presented is decided by the manufacturers, in a way they best decide would benefit consumers, rather than prescribed by the regulator.

Product summaries must be provided in good time before the product is made available to retail investors. If the entity is listed, whilst it remains listed, this means that an up-to-date summary must be available at all times.

Other requirements of the CCI regulations include that the document must be standalone separate from other marketing materials, sufficient individually to understand the nature and risks of a product, and that the summary is reviewed regularly, at least annually. It is also recommended that the document be reviewed when there is a material change to the company's investment objectives or strategy, or a market event occurs that affects the risk and return profile. As with the formatting requirements, the onus is very much on manufacturers to produce and manage the document how they best see fit for their target audience, but the rationale for their approach must be documented and be reasonable. Manufactures are also required to keep records of each version of their product summary for three years.

Manufacturer and Distributer Responsibilities

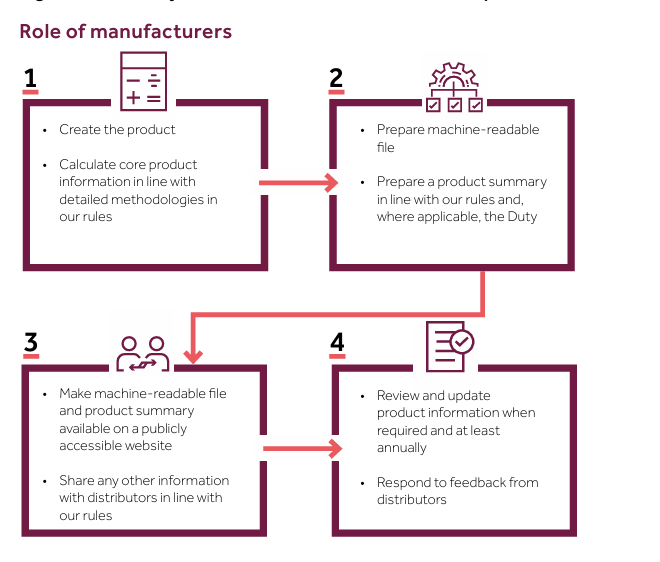

While manufacturers are primarily responsible for preparing and maintaining product summaries, this falls into a wider set of obligations under the CCI regulations.

The FCA sets outs its expectation of manufacturers as follows:

- Creating the product and calculating core product information;

- Preparing a product summary and machine-readable disclosure file in accordance with FCA rules;

- Making disclosures publicly available (e.g. via a website) and sharing them with distributors;

- Reviewing and updating disclosures at least annually; and

- Responding to distributor feedback regarding product communications.

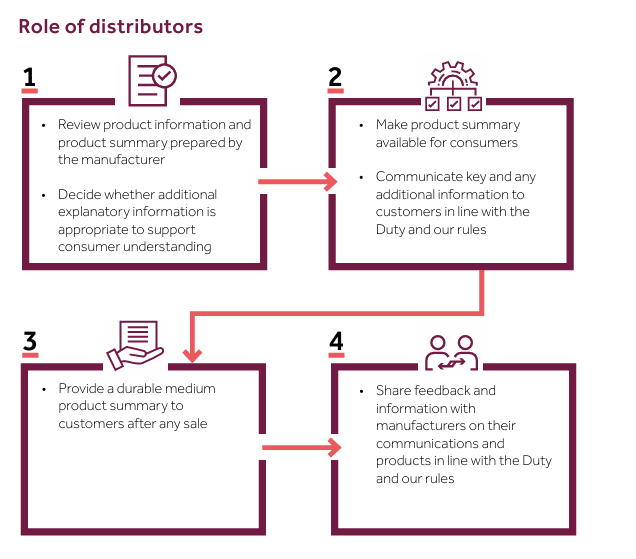

While a less onerous, but equally important role, distributors are required to work alongside manufacturers and are responsible for ensuring that product information reaches consumers effectively. In the context of VCTs and Investment Trusts, who regularly conduct secondary share issues, this will include any white label distributors and brokers they use to raise funds for them.

Their obligations include:

- Reviewing product summaries and assessing whether additional explanatory material is needed;

- Providing product summaries to customers at or before the point of sale;

- Highlighting key information, including:

- Product description;

- Costs and charges (ongoing and one-off);

- Risk rating;

- Key risks and warnings;

- Providing a product summary in a durable medium after sale; and

- Sharing feedback with manufacturers.

Distributors must not amend product summaries themselves but should instead provide feedback to the manufacturer where changes may be necessary.

The FCA in their guidance have provided these helpful flow charts setting out the responsibilities of both parties:

Next Steps for Companies

Although the CCI Regulations are not compulsory until 8 June 2027, it is advisable for some preparation to take place in advance of this to avoid a rushed transition. We recommend that companies should consider taking the following steps to prepare:

- Review all products and identify those that may qualify as CCIs targeting the UK market.

- Identify responsibilities as either a manufacturer or distributor and prepare processes to comply with new obligations.

Start to engage in the preparation process for the new CCI document, including appointing any necessary advisers to avoid that last minute rush towards full implementation next June.

This note is not intended to, nor seeks to replace, comprehensive advice on the new CCI regime, but is simply an overview. Howard Kennedy would be delighted to discuss any element of the new CCI regime with you and provide tailored support through the transition. Please contact Keith Lassman or Marc Proudfoot should you have any queries.

/Passle/5ae984fe7bae7607b4016f47/SearchServiceImages/2026-07-16-14-39-41-308-6a58ed2dea2dd4e542db12ee.jpg)